A superbill is one of the most important documents in medical billing, yet many patients and healthcare providers are unfamiliar with how it works. Whether you’re seeking reimbursement for out-of-network care or managing billing operations for a healthcare practice, understanding superbills can help streamline the payment process and reduce claim complications.

Unlike a standard invoice or receipt, a superbill contains essential medical billing information, including diagnosis codes (ICD-10), procedure codes (CPT), provider details, and treatment charges. Insurance companies use this information to evaluate reimbursement requests and determine eligible coverage.

In this article, you’ll learn what a superbill is, how it works, what information it includes, who needs it, and how to use it correctly to improve the chances of successful insurance reimbursement.

What Is a Superbill?

A superbill is a detailed medical billing document created by a healthcare provider after a patient receives treatment. It includes essential information such as diagnosis codes (ICD-10), procedure codes (CPT), provider details, and the cost of services rendered. Patients can submit this document to their insurance company to request reimbursement for eligible out-of-network healthcare expenses.

Unlike a standard receipt, a superbill contains the clinical and billing information insurers need to process reimbursement claims accurately.

Why Is It Called a Superbill?

The term “superbill” comes from its comprehensive nature. It combines medical, diagnostic, and billing information into a single document, making it much more detailed than an invoice or payment receipt.

Healthcare providers use superbills to document patient encounters and communicate treatment details in a format recognized by insurance companies. This allows insurers to determine whether the services qualify for reimbursement and how much they will cover.

Who Uses a Superbill?

Superbills are commonly used by healthcare providers who operate outside an insurance network and by patients seeking reimbursement for covered services.

Professionals who frequently issue superbills include:

- Physicians and medical specialists

- Psychologists and therapists

- Psychiatrists

- Chiropractors

- Physical therapists

- Occupational therapists

- Speech therapists

- Dietitians and nutritionists

Patients who visit out-of-network providers often rely on superbills to recover a portion of their healthcare expenses through their insurance plan.

What Is the Purpose of a Superbill in Medical Billing?

A superbill serves as a bridge between healthcare services and insurance reimbursement. It provides the documentation insurers need to evaluate a claim and determine whether a patient is eligible for compensation.

Without a properly completed superbill, insurance companies may lack the information necessary to process reimbursement requests.

Main Functions of a Superbill

A superbill performs several important roles within the medical billing process:

- Documents the medical services provided to the patient

- Records diagnosis and procedure codes

- Supports insurance reimbursement claims

- Maintains accurate patient billing records

- Helps providers track services and charges

It acts as an official record of treatment while ensuring billing information is organized and standardized.

Why Healthcare Providers Issue Superbills

Many healthcare professionals prefer issuing superbills because it allows them to focus on patient care without managing extensive insurance billing procedures.

By providing a superbill, providers can:

- Receive payment directly from patients

- Reduce insurance-related administrative tasks

- Simplify practice operations

- Support out-of-network reimbursement requests

This model is particularly common among private practices and mental health providers.

Benefits for Patients

For patients, a superbill offers the opportunity to receive reimbursement even when their provider is not contracted with their insurance company.

Key benefits include:

- Potential recovery of healthcare costs

- Access to a wider range of specialists

- Greater freedom in choosing providers

- Improved transparency regarding treatment charges

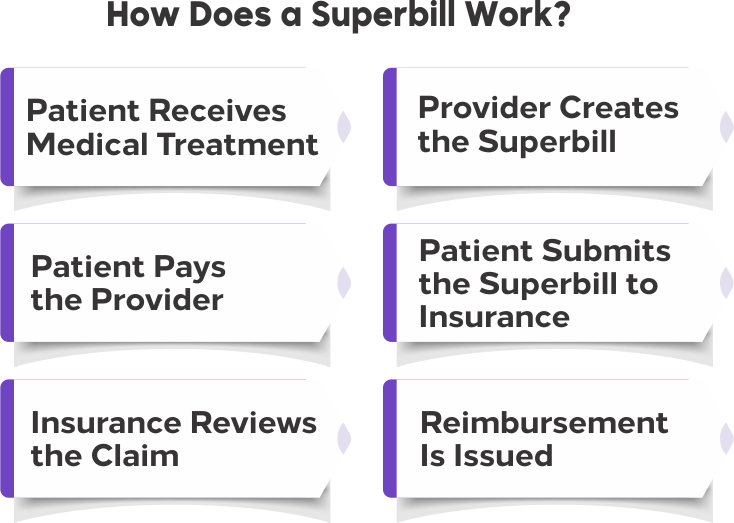

How Does a Superbill Work?

The superbill process is straightforward but requires accurate documentation and timely submission. Understanding each step can help patients avoid delays and improve reimbursement outcomes.

Step 1: Patient Receives Medical Treatment

The process begins when a patient receives healthcare services from a provider. This may include consultations, therapy sessions, evaluations, treatments, or follow-up visits.

Step 2: Provider Creates the Superbill

After the appointment, the provider generates a superbill containing all relevant billing and clinical information associated with the visit.

This includes:

- Patient information

- Provider credentials

- Diagnosis codes

- Procedure codes

- Service dates

- Charges

Step 3: Patient Pays the Provider

In most cases, the patient pays the provider directly at the time of service or according to the practice’s payment policy.

Because the provider is often out of network, payment is collected upfront rather than through direct insurance billing.

Step 4: Patient Submits the Superbill to Insurance

The patient then sends the superbill to their insurance company, either online, through a claims portal, or by mail.

Some insurers may also require additional claim forms or supporting documentation.

Step 5: Insurance Reviews the Claim

The insurance company reviews the superbill to verify:

- Coverage eligibility

- Medical necessity

- Diagnosis and procedure codes

- Reimbursement rules under the patient’s policy

Step 6: Reimbursement Is Issued

If the claim is approved, the insurance company reimburses the patient according to their out-of-network benefits, deductible requirements, and coverage limits.

The reimbursement amount varies based on the insurance plan and services received.

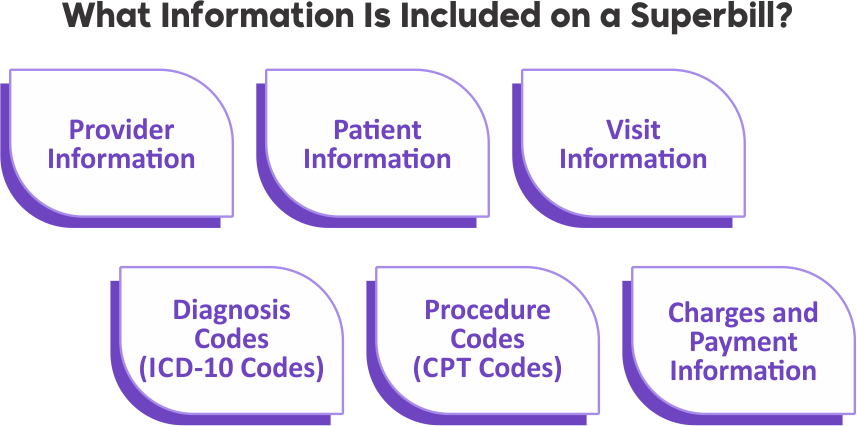

What Information Is Included on a Superbill?

A superbill must contain specific information to meet insurance reimbursement requirements. Missing or inaccurate details can result in claim delays or denials.

Provider Information

The document includes identifying details about the healthcare provider, such as:

- Provider name

- Practice name

- National Provider Identifier (NPI)

- Tax Identification Number (TIN or EIN)

- Practice address

- Contact information

These details allow insurance companies to verify the provider’s credentials and eligibility.

Patient Information

A superbill also includes patient-specific information, including:

- Full name

- Date of birth

- Address

- Insurance details

- Patient identification number (when applicable)

Accurate patient information helps insurers correctly associate the claim with the policyholder.

Visit Information

The superbill records details about the appointment itself, including:

- Date of service

- Type of visit

- Duration of treatment

- Location where services were provided

This information establishes when and where care was delivered.

Diagnosis Codes (ICD-10 Codes)

ICD-10 codes identify the medical condition, illness, injury, or reason for treatment.

Insurance companies use these codes to determine whether the services provided were medically necessary and covered under the patient’s plan.

Procedure Codes (CPT Codes)

CPT codes describe the specific medical services performed during the visit.

Examples may include:

- Office consultations

- Therapy sessions

- Physical examinations

- Diagnostic procedures

These codes help insurers calculate reimbursement amounts accurately.

Charges and Payment Information

The final section outlines the financial details of the visit, including:

- Cost of each service

- Total amount billed

- Amount paid by the patient

- Outstanding balance, if any

Accurate charge information is essential for reimbursement calculations.

Superbill Example: What Does a Superbill Look Like?

Although formats vary between healthcare providers, most superbills follow a similar structure and contain standardized billing information required by insurance companies.

A typical superbill includes provider details at the top, patient information, diagnosis and procedure codes, service dates, and a summary of charges.

Sample Superbill Breakdown

Below is a simplified example of the information commonly found on a superbill:

| Field | Example |

| Provider Name | ABC Medical Clinic |

| NPI Number | 1234567890 |

| Patient Name | John Smith |

| Date of Service | March 15 |

| ICD-10 Code | F41.1 |

| CPT Code | 90837 |

| Service Charge | $150 |

| Total Amount | $150 |

Why This Information Matters

Every field on a superbill serves a purpose. Insurance companies rely on diagnosis and procedure codes to determine coverage, while provider credentials and service details help verify the legitimacy of the claim.

A complete and accurate superbill significantly increases the likelihood of successful reimbursement and minimizes delays during claim processing.

Who Needs a Superbill?

Superbills are most commonly used by healthcare providers who operate outside insurance networks and by patients seeking reimbursement for covered services. While almost any medical professional can issue a superbill, certain specialties rely on them more frequently than others.

1. Mental Health Professionals

Mental health providers are among the most common users of superbills. Many therapists and counselors choose not to contract directly with insurance companies, allowing them to focus more on patient care and less on administrative tasks.

Professionals who often provide superbills include:

- Licensed therapists

- Clinical psychologists

- Counselors

- Psychiatrists

- Marriage and family therapists

Patients can use these superbills to seek reimbursement through their out-of-network mental health benefits.

2. Physical Therapy Clinics

Physical therapists frequently issue superbills when treating patients outside insurance networks. These documents help patients recover a portion of treatment costs while maintaining access to specialized care.

3. Chiropractic Practices

Many chiropractic clinics provide superbills to patients who want to submit claims independently. This approach simplifies billing while giving patients the flexibility to pursue reimbursement from their insurance provider.

4. Occupational and Speech Therapists

Occupational therapy and speech therapy providers also use superbills, especially in private practice settings where direct insurance billing may not be offered.

5. Dietitians and Nutritionists

As insurance coverage for nutritional counseling continues to expand, registered dietitians and nutritionists increasingly provide superbills to support reimbursement requests.

Why Superbills Are Popular in Private Practices

Private practices often prefer superbills because they:

- Reduce insurance-related paperwork

- Improve cash flow through direct patient payments

- Minimize claim management responsibilities

- Allow providers greater flexibility in treatment planning

For patients, this means access to a broader network of specialists without being limited to in-network providers.

Superbill vs Medical Claim: What’s the Difference?

Many people mistakenly believe a superbill and a medical claim are the same thing. While they are closely related, they serve different purposes within the reimbursement process.

| Feature | Superbill | Medical Claim |

| Created By | Healthcare Provider | Provider or Insurance Billing Team |

| Submitted By | Usually Patient | Usually Provider |

| Purpose | Supports Reimbursement Request | Requests Direct Insurance Payment |

| Payment Flow | Patient Pays First | Insurance Pays Provider Directly |

| Insurance Processing | Indirect | Direct |

What Makes a Superbill Different?

A superbill is not an insurance claim itself. Instead, it contains the information needed to create and support a claim.

Think of a superbill as the documentation behind a reimbursement request. It provides insurers with the diagnosis codes, procedure codes, provider credentials, and charges required to evaluate coverage.

When Is a Medical Claim Used?

Medical claims are typically used when a provider participates in an insurance network. The provider submits the claim directly to the insurance company and receives payment according to the patient’s benefits.

When Is a Superbill Used?

A superbill is generally used when:

- The provider is out of network

- The patient pays upfront

- The patient seeks reimbursement independently

Understanding this distinction helps patients navigate the reimbursement process more effectively.

Superbill vs Invoice vs Receipt

Although these documents all involve healthcare payments, they serve very different functions.

| Feature | Superbill | Invoice | Receipt |

| Includes CPT Codes | Yes | No | No |

| Includes ICD-10 Codes | Yes | No | No |

| Used for Insurance Reimbursement | Yes | No | Limited |

| Shows Services Provided | Yes | Sometimes | Sometimes |

| Proof of Payment | May Include | No | Yes |

What Is an Invoice?

An invoice is a request for payment issued by a healthcare provider. It outlines services rendered and the amount owed, but does not contain the coding information required by insurance companies.

What Is a Receipt?

A receipt confirms that payment has been made. While it may show the amount paid and date of service, it typically lacks diagnosis and procedure codes.

How to Submit a Superbill to Insurance?

Submitting a superbill correctly can improve the likelihood of reimbursement and reduce delays. While the exact process varies by insurance company, the overall steps remain similar.

Step 1: Verify Your Out-of-Network Benefits

Before submitting a superbill, review your insurance policy to determine:

- Whether out-of-network services are covered

- Deductible requirements

- Coinsurance percentages

- Reimbursement limits

Understanding your benefits helps set realistic reimbursement expectations.

Step 2: Gather Required Documents

Most insurance companies require more than just the superbill.

You may need:

- The completed superbill

- Member claim form

- Proof of payment

- Referral documentation (if required)

Step 3: Complete the Claim Form

Many insurers provide claim forms through their websites or member portals. Complete all requested fields accurately to avoid processing delays.

Step 4: Submit the Superbill

Depending on your insurer, you may submit documents through:

- Online member portals

- Mobile applications

- Email submission systems

- Traditional mail

Digital submission is often the fastest option.

Step 5: Monitor Claim Status

After submission, track your claim through the insurer’s portal or customer service department.

Keep copies of all documents in case additional information is requested.

Step 6: Appeal Denied Claims

If your claim is denied, review the explanation of benefits (EOB) to identify the reason.

Many denials can be resolved by:

- Correcting coding errors

- Providing additional documentation

- Submitting an appeal within the required timeframe

Common Reasons Superbills Get Rejected

Even minor errors can result in claim denials or reimbursement delays. Understanding common mistakes can help both patients and providers avoid unnecessary complications.

Missing Provider Information:

Insurance companies require complete provider credentials, including:

- NPI number

- Practice information

- Contact details

- Tax identification number

Missing information may cause automatic rejection.

Incorrect CPT Codes:

Procedure codes must accurately reflect the services performed. Incorrect coding can trigger denials, reduced reimbursement, or requests for additional review.

Invalid ICD-10 Diagnosis Codes:

Diagnosis codes must support the medical necessity of the treatment provided. Coding inconsistencies often lead to claim disputes.

Incomplete Patient Information:

Simple mistakes such as misspelled names, incorrect member IDs, or outdated insurance information can delay processing.

Missing Signatures or Documentation:

Some insurers require additional forms, proof of payment, or provider signatures before reviewing a claim.

Out-of-Network Coverage Limitations:

Not all insurance plans offer out-of-network benefits. In these situations, reimbursement may be denied regardless of how accurately the superbill is completed.

How to Avoid Reimbursement Delays?

To improve approval rates:

- Verify insurance benefits before treatment

- Ensure all codes are accurate

- Review patient information carefully

- Submit claims promptly

- Keep copies of all supporting documents

A well-prepared superbill significantly increases the chances of successful reimbursement while reducing administrative back-and-forth with insurance providers.

Benefits of Using a Superbill

Superbills offer advantages for both patients and healthcare providers. They simplify the reimbursement process while providing greater flexibility in how medical services are delivered and paid for.

Benefits for Patients

For patients, the biggest advantage of a superbill is the opportunity to receive reimbursement for out-of-network healthcare services.

Key benefits include:

- Access to preferred healthcare providers

- Potential reimbursement from insurance companies

- Greater flexibility in choosing specialists

- More transparency regarding treatment costs

- Access to services that may not be available in-network

Many patients use superbills to continue receiving care from trusted providers without being restricted by network limitations.

Benefits for Healthcare Providers

Providers also benefit from issuing superbills instead of managing direct insurance billing.

Some of the most significant advantages include:

- Reduced administrative burden

- Fewer insurance-related tasks

- Faster payment collection

- Improved cash flow

- Greater focus on patient care

Rather than waiting for insurance approvals, providers typically receive payment directly from patients at the time of service.

Benefits for Healthcare Practices

From a business perspective, superbills can help practices streamline operations and reduce billing complexities.

Advantages include:

- Simplified revenue collection

- Fewer claim disputes

- Lower billing overhead

- Reduced dependence on insurance networks

- Enhanced practice efficiency

For many private practices, this approach creates a more predictable and manageable revenue cycle.

Challenges and Limitations of Superbills

While superbills provide numerous benefits, they are not without limitations. Patients should understand the potential drawbacks before relying on out-of-network reimbursement.

Insurance Approval Is Not Guaranteed

Submitting a superbill does not automatically result in reimbursement.

Insurance companies evaluate factors such as:

- Plan benefits

- Medical necessity

- Coverage limitations

- Deductible requirements

As a result, reimbursement amounts can vary significantly.

Patients Must Pay Upfront

Unlike direct insurance billing, patients are usually responsible for paying the full service fee before seeking reimbursement.

This can create short-term financial challenges for some individuals.

Reimbursement Amounts May Be Lower Than Expected

Insurance companies often reimburse based on their allowable amount rather than the provider’s actual charge.

Patients may remain responsible for the difference between:

- Provider fees

- Insurance reimbursement

This is commonly referred to as balance billing.

Manual Claim Submission

Some insurers still require patients to complete forms and submit documentation manually.

This process can involve:

- Additional paperwork

- Follow-up communication

- Longer processing times

Coding Errors Can Affect Reimbursement

Incorrect diagnosis or procedure codes may result in:

- Claim denials

- Delayed processing

- Reduced reimbursement amounts

Accurate coding remains essential for successful claim outcomes.

Can You Create a Superbill Electronically?

Yes. Most healthcare providers now generate electronic superbills through medical billing software and electronic health record (EHR) systems.

Digital superbills improve accuracy, reduce paperwork, and simplify reimbursement submissions.

Electronic Health Record (EHR) Integration

Modern EHR systems automatically capture patient and treatment information, making superbill creation faster and more accurate.

These systems can populate:

- Patient demographics

- Provider information

- Diagnosis codes

- Procedure codes

- Service dates

This reduces manual data entry and minimizes errors.

Automated Superbill Generation

Many medical billing platforms can automatically generate a superbill immediately after a patient visit.

Automation helps practices:

- Save time

- Improve coding accuracy

- Reduce administrative workload

- Maintain compliance standards

HIPAA Compliance Considerations

Because superbills contain protected health information (PHI), providers must ensure that electronic documents are handled securely.

Best practices include:

- Encrypted storage

- Secure patient portals

- Access controls

- HIPAA-compliant software solutions

Protecting patient information is critical throughout the billing process.

Popular Software Used for Superbills

Many healthcare practices rely on specialized platforms to generate and manage superbills, including:

- Kareo

- AdvancedMD

- SimplePractice

- TherapyNotes

- Athenahealth

- DrChrono

- NextGen Healthcare

These platforms help streamline billing workflows while maintaining compliance requirements.

Superbill Requirements by Insurance Company

One question patients frequently ask is whether every insurance company accepts superbills. The answer depends on the specific plan and its out-of-network coverage policies.

Do All Insurance Companies Accept Superbills?

Most major insurance providers accept superbills for reimbursement requests when a plan includes out-of-network benefits.

However, acceptance does not guarantee reimbursement.

Coverage depends on factors such as:

- Policy terms

- Deductible status

- Medical necessity

- Service eligibility

- Reimbursement limits

Major Insurance Carriers That Commonly Process Superbills

Many patients submit superbills to insurers such as:

- Aetna

- UnitedHealthcare

- Cigna

- Blue Cross Blue Shield

- Humana

- Kaiser Permanente (plan-dependent)

Each insurer maintains its own reimbursement procedures and documentation requirements.

Important Considerations Before Submission

Before submitting a superbill, patients should verify:

- Whether out-of-network services are covered

- Submission deadlines

- Required claim forms

- Documentation requirements

- Reimbursement percentages

Contacting the insurance company beforehand can help avoid unexpected claim denials and reimbursement delays.

How Long Does It Take to Get Reimbursed From a Superbill?

One of the most common questions patients ask after submitting a superbill is how long reimbursement will take. While timelines vary by insurance provider, most claims are processed within a few weeks.

Average Reimbursement Timeline

In most cases, insurance companies process superbill claims within:

- 2 to 6 weeks for electronic submissions

- 4 to 8 weeks for mailed submissions

- Longer if additional documentation is requested

Some insurers may process claims faster, while others require more extensive review.

Can Medicare and Medicaid Accept Superbills?

Medicare and Medicaid operate differently from many commercial insurance plans, so reimbursement rules may vary depending on the provider and service received.

1. Medicare and Superbills

In some situations, Medicare beneficiaries may receive documentation similar to a superbill. However, Medicare generally follows strict billing requirements.

Factors that influence reimbursement include:

- Whether the provider participates in Medicare

- Type of service received

- Medicare coverage rules

- Assignment status of the provider

Patients should verify eligibility directly with Medicare or their provider before assuming reimbursement is available.

2. Medicaid and Superbills

Medicaid policies differ by state, making reimbursement rules more complex.

In many cases:

- Medicaid requires participating providers

- Out-of-network reimbursement may be limited

- Prior authorization requirements may apply

Patients covered by Medicaid should contact their state Medicaid agency for specific guidance.

Summary

A superbill is a critical document in medical billing that helps patients seek reimbursement for eligible out-of-network healthcare services. Including essential details such as provider information, diagnosis codes, procedure codes, and treatment charges, it gives insurance companies the information needed to evaluate and process claims.

Whether you’re a patient looking to recover healthcare expenses or a provider seeking a simpler billing process, understanding how superbills work can help you avoid common mistakes and improve reimbursement success. From accurate coding and proper documentation to timely claim submission, every step plays a role in ensuring a smoother insurance reimbursement experience.

When used correctly, a superbill can bridge the gap between out-of-network care and insurance coverage, making healthcare payments more transparent and manageable for everyone involved.