Workers’ compensation insurance is a legal requirement for many businesses, but not every worker or business owner is required to carry coverage. Understanding who qualifies for an exemption can help employers avoid costly compliance mistakes, reduce unnecessary insurance expenses, and make informed hiring decisions.

From independent contractors and sole proprietors to corporate officers and agricultural workers, exemption rules vary widely based on business structure, job classification, and state regulations.

Knowing where these exceptions apply and where they don’t is essential for protecting your business from penalties, lawsuits, and unexpected financial risks.

What Is Workers’ Compensation Insurance?

Workers’ compensation insurance is a type of coverage that provides financial support to employees who suffer work-related injuries or illnesses. In exchange for these benefits, employees generally waive their right to sue their employer for workplace injuries.

For employers, workers’ compensation is more than just an insurance policy—it is often a legal requirement designed to protect both businesses and workers from the financial consequences of workplace accidents.

What Does Workers’ Compensation Cover?

A standard workers’ compensation policy typically covers:

- Medical treatment and hospital expenses

- Rehabilitation and physical therapy costs

- Lost wages during recovery

- Disability benefits for temporary or permanent injuries

- Death benefits for dependents in fatal workplace accidents

Coverage applies regardless of who caused the accident in most cases, making it a crucial safety net for employees.

Who Is Usually Required to Carry Workers’ Compensation Insurance?

Most states require employers to carry workers’ compensation insurance as soon as they hire one or more employees. However, employee thresholds and coverage requirements vary by state.

Businesses that fail to maintain required coverage may face substantial fines, stop-work orders, lawsuits, and even criminal penalties in some jurisdictions.

Who Is Exempt From Workers’ Compensation Insurance?

The answer depends largely on state law, business structure, and worker classification. While most employees are protected under workers’ compensation laws, several groups are commonly exempt from mandatory coverage requirements.

Common Workers’ Compensation Exemptions

Workers who may qualify for exemptions include:

- Independent contractors

- Sole proprietors

- Business partners

- Certain LLC members

- Corporate officers

- Agricultural workers

- Domestic workers

- Volunteers

- Family members working in family-owned businesses

- Certain seasonal and casual workers

It is important to understand that an exemption in one state may not apply in another. Employers should always verify requirements with their state’s workers’ compensation authority before assuming coverage is unnecessary.

1. Independent Contractors

Independent contractors are among the most commonly exempt workers under workers’ compensation laws. Since they operate as self-employed individuals rather than employees, businesses are generally not required to provide workers’ compensation coverage for them.

Why Independent Contractors Are Usually Exempt

Independent contractors typically:

- Control how their work is performed

- Use their own tools and equipment

- Work for multiple clients

- Receive a Form 1099 instead of a W-2

Because they operate independently, they are generally responsible for obtaining their own insurance coverage if desired.

When Contractors May Still Need Coverage

Being classified as an independent contractor does not automatically eliminate workers’ compensation obligations.

Certain industries, particularly construction, trucking, and government contracting, may require contractors to carry their own workers’ compensation policy before they can work on a project.

Some clients also require proof of coverage to reduce liability risks.

Misclassification Risks for Employers

One of the most expensive mistakes employers make is classifying employees as independent contractors solely to avoid insurance costs.

If a state agency determines that a worker was actually an employee, the employer may face:

- Backdated insurance premiums

- Tax penalties

- Regulatory fines

- Employee injury claims

- Legal disputes

Proper worker classification is essential for compliance and risk management.

2. Sole Proprietors and Self-Employed Individuals

Sole proprietors and self-employed professionals are often exempt from mandatory workers’ compensation requirements because they are not considered employees of their own businesses.

Are Sole Proprietors Exempt?

In many states, sole proprietors can choose whether to purchase workers’ compensation coverage. This exemption allows business owners to avoid paying premiums when coverage is not legally required.

However, some states require owners to file formal exemption paperwork if they wish to opt out.

Why Many Self-Employed Workers Purchase Coverage Anyway

Even when coverage is optional, many self-employed professionals choose to carry workers’ compensation insurance because workplace injuries can create significant financial hardship.

Benefits may include:

- Medical expense protection

- Income replacement during recovery

- Reduced financial stress

- Increased credibility with clients

A single workplace injury can result in thousands of dollars in unexpected costs, making voluntary coverage a worthwhile investment for many business owners.

Industries Where Coverage Is Common

Self-employed professionals commonly purchase workers’ compensation coverage in industries such as:

- Construction

- Roofing

- Electrical work

- Plumbing

- Trucking

- Landscaping

In many cases, clients and general contractors require proof of insurance before awarding contracts.

3. Partners, LLC Members, and Business Owners

Business owners often qualify for workers’ compensation exemptions, but eligibility depends on how the company is structured.

Partnership Exemptions

Partners in a partnership are commonly exempt because they are considered owners rather than employees. As a result, workers’ compensation coverage is frequently optional unless the partnership hires additional employees.

LLC Member Exemptions

Many states allow LLC members to opt out of workers’ compensation coverage. However, the rules differ significantly based on ownership percentages and state regulations.

Some states automatically exempt LLC members, while others require a formal election process.

Corporate Officer Exemptions

Corporate officers may also qualify for exemptions under certain conditions. States often impose ownership thresholds or require officers to submit exemption forms before opting out.

Can Business Owners Choose Coverage?

Yes. Even if business owners qualify for an exemption, many insurance providers allow them to voluntarily include themselves in a workers’ compensation policy.

This option can provide valuable protection against medical costs and lost income resulting from workplace injuries, especially in high-risk industries.

4. Corporate Officers and Executives

Corporate officers are often treated differently from regular employees under workers’ compensation laws. In many states, qualifying officers can choose to exempt themselves from coverage, helping reduce insurance costs for the business.

Which Corporate Officers Can Be Exempt?

Depending on state regulations, exemptions may apply to:

- Company presidents

- Vice presidents

- Secretaries

- Treasurers

- Other executive officers with ownership interests

However, eligibility requirements vary significantly. Some states require officers to own a minimum percentage of the company before they can opt out.

Ownership Requirements Matter

Many states use ownership thresholds to determine exemption eligibility. For example, a corporate officer who owns a substantial share of the business may qualify for an exemption, while a non-owner executive may still be treated as an employee for workers’ compensation purposes.

Should Corporate Officers Opt Out?

Although exempting officers can reduce premium expenses, it may also leave them financially exposed if a workplace injury occurs. Business owners should carefully evaluate the risks before declining coverage.

Workers Commonly Exempt by Industry

Beyond business owners and contractors, certain occupations and industries often receive special treatment under workers’ compensation laws.

Agricultural Workers

Many states provide exemptions for certain agricultural and farm workers, particularly on small farms with limited numbers of employees.

The reasoning is often tied to the seasonal nature of agricultural work and the financial burden that mandatory coverage could place on small farming operations.

Domestic Workers

Domestic employees may be exempt in some states, especially when they work limited hours or earn below specific wage thresholds.

Examples include:

- Nannies

- Housekeepers

- Babysitters

- Caregivers

- Gardeners

However, larger household employers may still be required to provide coverage.

Seasonal and Casual Workers

Workers hired temporarily or on an occasional basis may qualify for exemptions depending on state law and the nature of their employment.

Common examples include:

- Holiday staff

- Temporary event workers

- Short-term laborers

Volunteers

Because volunteers generally do not receive wages, they are often excluded from mandatory workers’ compensation requirements.

This commonly applies to:

- Charitable organizations

- Religious institutions

- Community programs

Some organizations still choose to provide coverage voluntarily to protect volunteers.

Family Members in Family-Owned Businesses

Certain states exempt immediate family members working within a family-owned business. This exemption is particularly common among small businesses, farms, and closely held companies.

Federal Employees and Other Special Exceptions

Not all workers fall under state workers’ compensation systems. Certain occupations are covered through separate federal programs specifically designed for their industries.

Federal Employees

Federal government employees are generally covered through federal compensation programs rather than state workers’ compensation systems.

These programs provide benefits for:

- Workplace injuries

- Occupational illnesses

- Disability claims

- Survivor benefits

Railroad Workers

Railroad employees are typically covered under specialized federal laws that differ from traditional workers’ compensation programs.

Unlike standard workers’ compensation systems, some railroad injury claims may involve proving employer negligence.

Maritime and Longshore Workers

Employees who work on navigable waters, docks, ports, and shipping facilities often receive protection through specialized maritime compensation programs.

These programs address the unique risks associated with marine and waterfront employment.

Why These Exceptions Exist

Federal and industry-specific compensation systems were created because certain occupations face unique workplace hazards that are not adequately addressed by traditional state workers’ compensation laws.

Understanding these exceptions is important for employers operating in transportation, maritime, logistics, and government sectors.

State-by-State Workers’ Compensation Exemptions

One of the biggest mistakes employers make is assuming workers’ compensation rules are the same nationwide. In reality, every state establishes its own requirements, exemptions, and employee thresholds.

Why State Laws Matter

A worker who qualifies for an exemption in one state may require coverage in another. Similarly, a business owner who can opt out in one jurisdiction may be required to participate in another.

Factors that vary by state include:

- Minimum employee thresholds

- Owner exemption rules

- Contractor requirements

- Agricultural worker exemptions

- Domestic worker exemptions

- Corporate officer elections

Examples of State Differences

| State | Coverage Requirement | Notable Exemptions |

| California | Generally required with one employee | Limited owner exemptions |

| Florida | Varies by industry | Certain corporate officers and owners |

| Texas | Most private employers are not required to carry coverage | Unique non-subscriber system |

| Georgia | Required for businesses with three or more employees | Some owner exemptions |

| Tennessee | Generally required for businesses with five or more employees | Certain business owners |

Because exemption laws frequently change, employers should review their state’s current requirements before making coverage decisions.

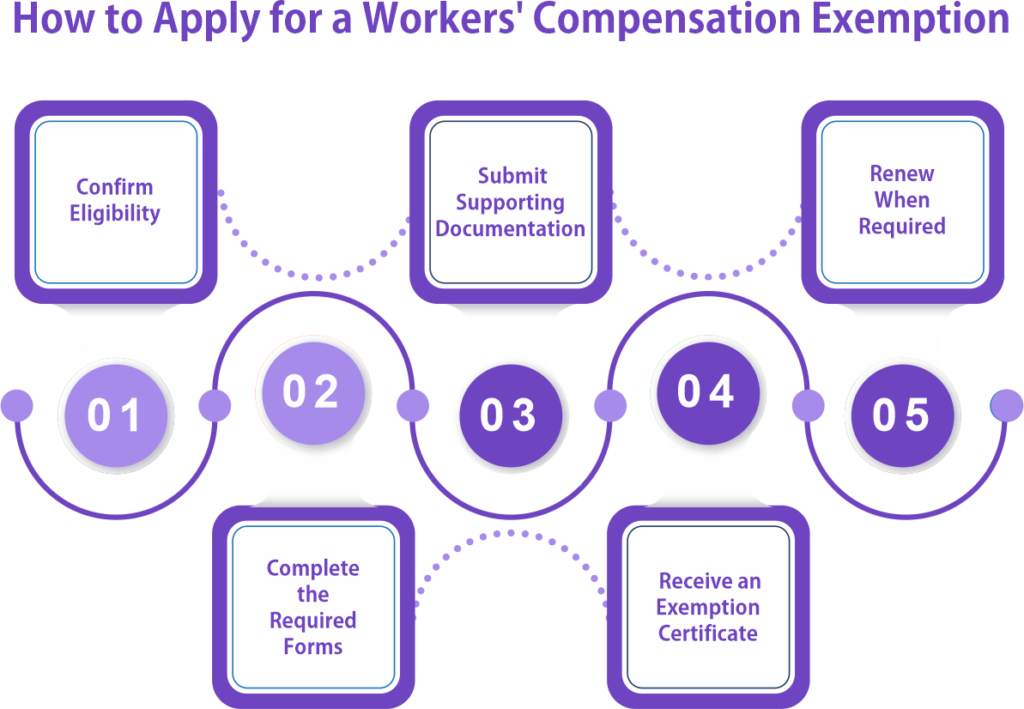

How to Apply for a Workers’ Compensation Exemption

Qualifying for an exemption does not always mean you are automatically exempt. Many states require business owners and eligible workers to complete a formal exemption process.

Step 1: Confirm Eligibility

Before applying, determine whether your business structure and role qualify under state law.

Commonly eligible applicants include:

- Sole proprietors

- Partners

- LLC members

- Corporate officers

Step 2: Complete the Required Forms

Most states require an exemption application or election form. The information requested may include:

- Business registration details

- Ownership information

- Identification documents

- Corporate records

Step 3: Submit Supporting Documentation

Applicants may need to provide proof of ownership or other records verifying their exemption eligibility.

Step 4: Receive an Exemption Certificate

Once approved, the state may issue an exemption certificate that serves as official proof of exempt status.

Many contractors and business owners provide this certificate to clients, general contractors, and government agencies when requested.

Step 5: Renew When Required

Some exemptions remain active indefinitely, while others require periodic renewal. Failing to renew an exemption may result in compliance issues and unexpected insurance obligations.

For this reason, business owners should monitor expiration dates and maintain accurate records of all exemption filings.

What Happens If You Incorrectly Claim an Exemption?

Claiming a workers’ compensation exemption without meeting the legal requirements can expose a business to serious financial and legal consequences. Many employers mistakenly assume that a worker qualifies as exempt, only to discover otherwise during an audit, injury claim, or government investigation.

Financial Penalties

States can impose substantial fines on businesses that fail to maintain required workers’ compensation coverage.

Potential penalties may include:

- Civil fines

- Backdated insurance premiums

- Interest charges

- Administrative fees

In some cases, penalties can exceed the cost of maintaining proper coverage for several years.

Stop-Work Orders

Many states have the authority to issue stop-work orders against non-compliant businesses.

This can result in:

- Project delays

- Lost revenue

- Contract cancellations

- Damage to business reputation

For industries such as construction, a stop-work order can be financially devastating.

Increased Liability Exposure

Workers’ compensation laws generally protect employers from employee injury lawsuits. However, if required coverage is not in place, injured workers may have the right to sue the employer directly.

This can lead to:

- Medical expense claims

- Lost wage claims

- Pain and suffering damages

- Legal defense costs

The financial impact of a lawsuit can far exceed the cost of workers’ compensation insurance.

Criminal Consequences

In some jurisdictions, intentionally avoiding workers’ compensation requirements may result in criminal penalties, including misdemeanor or felony charges.

Business owners should never assume an exemption applies without verifying eligibility under state law.

Should Exempt Workers Still Carry Workers’ Compensation Insurance?

Being exempt from workers’ compensation requirements does not necessarily mean coverage is unnecessary. Many exempt workers voluntarily purchase coverage to protect themselves and their businesses.

Benefits of Voluntary Coverage

Even when not legally required, workers’ compensation insurance can provide valuable financial protection.

Potential benefits include:

- Coverage for medical expenses

- Wage replacement during recovery

- Protection against unexpected injuries

- Improved business credibility

- Compliance with client contract requirements

For many self-employed professionals, the cost of coverage is relatively small compared to the financial consequences of a serious injury.

Industries Where Voluntary Coverage Makes Sense

Voluntary coverage is especially common in higher-risk industries such as:

- Construction

- Roofing

- Electrical work

- Plumbing

- Trucking

- Landscaping

- Manufacturing

Workers in physically demanding jobs often face a greater likelihood of workplace injuries, making coverage a practical investment.

Meeting Client Requirements

Many clients, property owners, and general contractors require proof of workers’ compensation insurance before allowing work to begin.

Even exempt business owners may purchase coverage solely to qualify for larger projects and contracts.

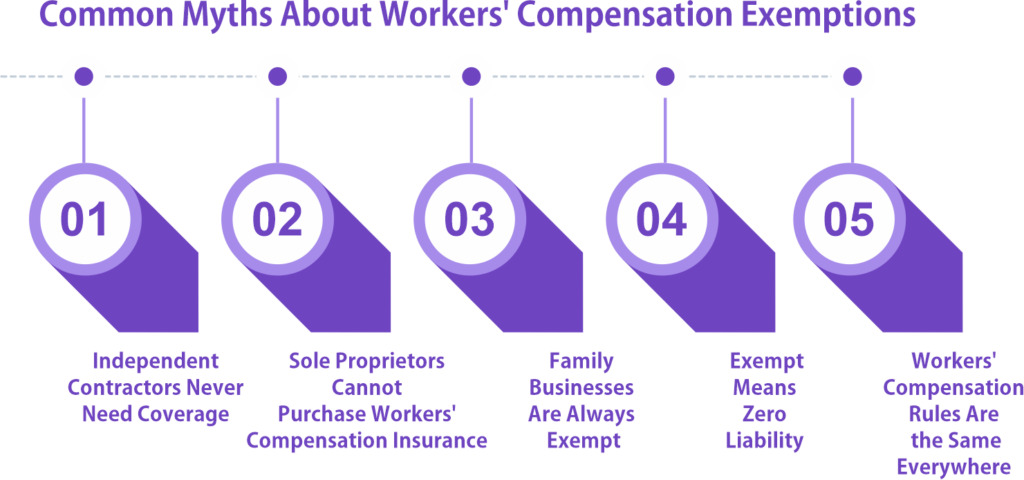

Common Myths About Workers’ Compensation Exemptions

Workers’ compensation exemptions are often misunderstood. Believing the wrong information can lead to compliance problems and costly mistakes.

Myth #1: Independent Contractors Never Need Coverage

Reality: While independent contractors are often exempt, certain industries, contracts, and state laws may still require coverage.

Myth #2: Sole Proprietors Cannot Purchase Workers’ Compensation Insurance

Reality: Most states allow sole proprietors to voluntarily purchase workers’ compensation coverage, even when they are exempt from mandatory participation.

Myth #3: Family Businesses Are Always Exempt

Reality: Some states exempt family members, while others require coverage depending on the relationship, ownership structure, and number of employees.

Myth #4: Exempt Means Zero Liability

Reality: Exemption from workers’ compensation requirements does not eliminate all business risks. Injuries can still lead to medical expenses, lost income, lawsuits, and contractual disputes.

Myth #5: Workers’ Compensation Rules Are the Same Everywhere

Reality: Every state has different laws regarding exemptions, employee thresholds, and coverage requirements.

Employers should never rely on information that applies to another state without verifying local regulations.

Key Takeaways

Workers’ compensation insurance is mandatory for many employers, but several categories of workers and business owners may qualify for exemptions. Common exemptions include independent contractors, sole proprietors, partners, certain LLC members, corporate officers, agricultural workers, volunteers, and some domestic workers.

Because exemption laws vary by state, employers should never assume an exemption applies without verifying local requirements. Incorrectly claiming an exemption can result in fines, lawsuits, stop-work orders, and significant financial losses.